Calculating the annuity formula is a valuable skill when planning for longterm financial goals, such as saving for retirement or paying off debts. The main idea behind an annuity is to help you figure out the value of a series of regular payments made over time, either as a lump sum today or in future value. In this article, I’ll guide you through the basics of how an annuity works, when and why you’d use annuity formulas, and how to calculate them easily—even if your math skills are rusty. Understanding these formulas can help you make smart choices about your financial future.

Understanding Annuities and Why the Formula Matters

An annuity is a financial product or arrangement where you pay (or receive) a series of equal payments spaced out over regular intervals. These are used in retirement accounts, insurance payouts, personal loans, or even savings plans. Unlike a single lump sum payment, annuities let you spread out the impact of a financial decision across a period of time. Knowing how to calculate the present value or future value of these payments helps you compare your options and make smarter financial decisions.

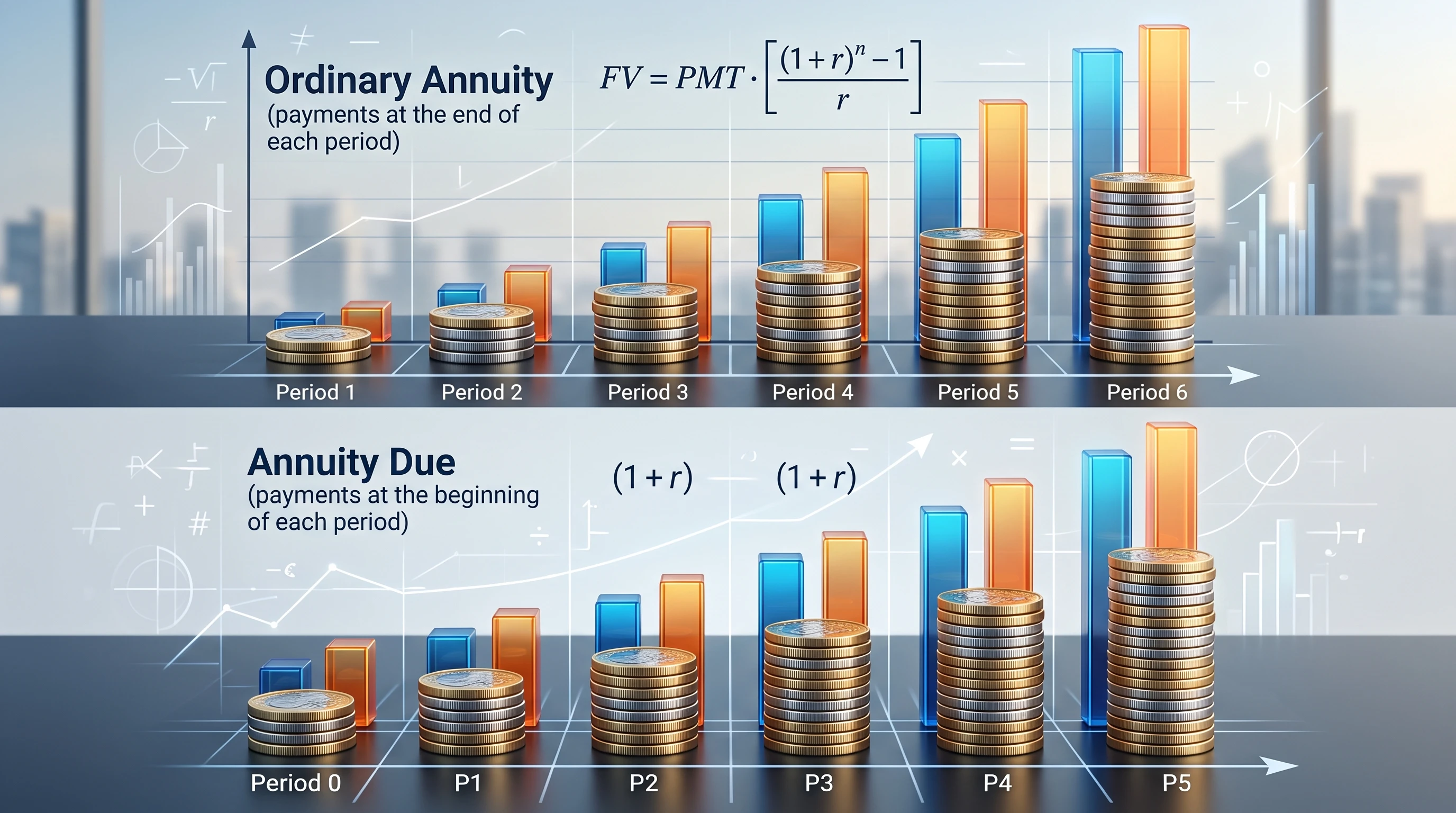

Annuities can be grouped into two main types: ordinary annuities and annuities due. Ordinary annuities pay at the end of each interval (for example, the end of the month), while annuities due pay at the beginning. This difference has a real impact when you’re working out how much an investment or set of payments is worth with formulas. Most bank loans and retirement savings accounts (such as a 401(k)) are ordinary annuities. Rent and lease payments, in contrast, are usually annuities due since payment happens at the start of a period.

People often stumble upon annuities in more ways than they realize, whether signing up for a gym membership with annual fees, investing in bonds that make regular coupon payments, or considering income options for retirement. Understanding how and when money enters or leaves your account is a big part of good financial planning.

Basic Terms and Concepts You Need to Know

Anyone learning to calculate annuity formulas will run into some financial terms. Here are a few of the key ones I use and what they mean in plain English:

- Present Value (PV): How much future payments are worth in today’s dollars.

- Future Value (FV): The total sum that repeated payments will reach in the future, given a certain interest rate.

- Interest Rate (r): The rate used to discount or grow payments over time; sometimes called the discount rate or return rate.

- Payment (PMT): The fixed amount paid or received in each period.

- Number of Periods (n): How many payments you’ll make or receive.

Getting a strong grip on these ideas is really important because they show up in every annuity calculation. Seeing these same terms repeatedly might feel repetitive, but it helps to reinforce what each one means. When comparing accounts or loans, always check if the payment amounts, frequency, and rates match up to your expectations.

How Do You Calculate Present Value for an Annuity?

Most people jumping into annuities start with the present value formula. Present value tells you what a stream of future cash flows is worth today, given a particular interest rate. Here’s the formula for an ordinary annuity (payments at the end of each period):

Present Value of an Ordinary Annuity:

PV = PMT × [1 – (1 + r)-n] / r

For example, suppose you want to know how much you should invest today if you want to receive $500 every year for 10 years, at a 5% annual return. Plug in the numbers:

- PMT = $500

- r = 0.05

- n = 10

PV = 500 × [1 – (1 + 0.05)-10] / 0.05

This calculation shows you the lump sum you’d need today to receive $500 per year for 10 years, with your money growing at a 5% interest rate.

Present Value for Annuity Due

If payments happen at the start of each period (annuity due), multiply the result by (1 + r):

PV (Annuity Due) = PV (Ordinary Annuity) × (1 + r)

This adjustment covers the benefit of receiving money sooner and lets your money earn more interest through an extra period for each payment.

How Do You Calculate Future Value for an Annuity?

While present value looks at what future money is worth today, future value tells you how much your regular payments will total by the end of the payment schedule. Here’s the formula for ordinary annuities:

Future Value of an Ordinary Annuity:

FV = PMT × [(1 + r)n – 1] / r

Suppose you save $200 a month for 15 years in a retirement account earning 6% interest (compounded yearly, for example). Plug in:

- PMT = $2,400 (since $200 per month × 12 months per year)

- r = 0.06

- n = 15

FV = 2,400 × [(1 + 0.06)15 – 1] / 0.06

This shows the total amount saved after 15 years, including compounded interest. Trying different amounts or rates can really open your eyes to how powerful compound interest can be over time.

Future Value for Annuity Due

As with the present value, if your payments come at the start of the period, multiply the result by (1 + r):

FV (Annuity Due) = FV (Ordinary Annuity) × (1 + r)

StepbyStep Guide to Calculating the Annuity Formula

Calculating an annuity formula sounds intimidating at first, but once you break it down, it gets a lot easier. Here’s how I recommend getting started:

- Identify the Type of Annuity: Figure out if the payments are at the start or end of the period. Knowing this helps you pick the correct formula every time.

- Gather Your Inputs: List out the PMT, interest rate, and number of periods you’ll be using. Getting these values right up front saves headaches later.

- Convert the Interest Rate if Needed: Ensure the rate matches your payment periods (monthly, yearly, etc.). For monthly payments, divide the annual rate by 12 to get the rate per period.

- Plug Values into the Formula: Use the right formula for your annuity type—ordinary or due.

- Calculate Using the Right Tools: For bigger, trickier numbers, a financial calculator or spreadsheet makes calculation quick and mistakefree.

This stepbystep method covers both present value and future value, and is useful for loans, savings plans, or structured payouts like settlements and pensions.

Common Applications of Annuity Formulas

Knowing annuity formulas has a real practical side. Here are some ways I’ve seen these formulas come up in daytoday life:

- Retirement Savings: Calculating how much to save each month to reach a target nest egg. This lets you set achievable, specific savings goals.

- Loan Repayment: Figuring out fixed monthly payments on a mortgage or car loan so you can budget and plan ahead.

- Lottery Winnings or Legal Settlements: Weighing the lump sum versus regular payments—formulas help you see which option is more valuable today.

- Insurance Payouts: Comparing a oneoff payment to getting smaller payments over several years. This can affect your taxes and cash flow management.

Understanding these scenarios can help you track down deals that maximize value and give you peace of mind with big financial choices.

Types of Annuities and How Formulas Might Change

The main formulas above work for fixedrate, regular payment annuities. In certain situations, formulas change just a little:

- Increasing or Growing Annuities: Payments go up by a fixed percentage each period instead of staying the same. This accounts for things like inflation adjustments in pensions. The formula adds a “growth rate” (g) element and is used when you want your income to rise over time.

- Perpetuities: An annuity that pays forever, such as some trust funds or endowments. The formula here is much simpler: PV = PMT / r because payments never end.

Most people just starting out rarely use these advanced types unless they’re dealing with major financial planning, trusts, or institutional investments.

Helpful Tips and Common Pitfalls to Watch Out For

Using annuity formulas is pretty straightforward once you’re comfortable with the steps, but it’s easy to run into small mistakes that can become costly over time. Here are several things to pay attention to:

- Mismatched Rates and Payment Periods: Don’t use an annual interest rate with monthly payments; always make sure the rate matches payment frequency.

- Adjusting for Annuity Due: For payments at the start of each period, remember the (1 + r) multiplier so your final answer is correct.

- Compound versus Simple Interest: Annuity formulas count on compound interest—not simple interest. Don’t mix the two up.

- Counting Periods Accurately: Doublecheck the total number of periods to make sure you include all payments.

Using calculators or spreadsheets is a great way to doublecheck your answers and prevent miscalculations. Even one small input error can derail a longterm savings or loan plan.

Using Calculators and Spreadsheet Functions

I find it massively helpful to check my work using an online annuity calculator (many banks and investment websites offer these for free) or Excel and Google Sheets. There are built-in spreadsheet functions, such as:

- =PV(rate, nper, pmt, [fv], [type]) for present value

- =FV(rate, nper, pmt, [pv], [type]) for future value

- Use 1 for the type if payments happen at the beginning (annuity due) and 0 if they happen at the end (ordinary annuity).

Taking advantage of these built-in features can really speed things up and helps you catch mistakes. I often enter the numbers one way by hand and then let the spreadsheet do the work to make sure everything matches up.

Important Things to Consider Before Using the Annuity Formula

Before relying on an annuity formula, I always reflect on a few real-world issues that can make a difference:

- Interest Rate Assumptions: Interest rates in real life can rise or fall, which can impact the outcome of your calculations. Don’t just guess—use reasonable, reliable numbers.

- Inflation: Over time, inflation will lower the buying power of your future payments. A $1,000 payment a decade from now probably won’t stretch as far as it does today.

- Fees and Taxes: Account for any admin fees or taxes that come with your investment—these aren’t in the standard formulas and can affect your actual returns.

- Payment Frequency and Compounding: Different products compound interest at different intervals, so verify how yours works before running the numbers. For instance, bank accounts might compound monthly, while bonds might do so annually.

Factoring in these elements helps you set realistic goals and avoid surprises. It also allows you to compare options more honestly, sidestepping results that look great in theory but don’t pan out in real life.

Advanced Tips for Making the Most of Annuity Calculations

Once you’re confident with annuity basics, there’s room to level up your strategy for even stronger financial planning:

DoubleCheck Your Answers: Always back up your hand calculations with a spreadsheet or calculator. Small mistakes can add up quickly and change your plans substantially.

Use Realistic Interest Rates: Plugging in optimistic rates gives pretty projections, but using moderate, down-to-earth returns will serve you better in the long run. It’s better to be pleasantly surprised than to overpromise and underdeliver.

Review Your Plans Each Year: Life and the market change fast. I like to revisit my calculations at least annually. This keeps your plan up-to-date if you get a new job, face unexpected expenses, or if interest rates jump or drop.

Check in with Professionals if Unsure: Even with handy tools, sometimes you might get stuck. Financial advisors, helpful calculators, or even someone at your bank can confirm if you’re on the right track.

Frequently Asked Questions

People often ask about annuity formulas while getting their finances in order. Here are a few common questions and straightforward answers:

Question: Can I use the annuity formula for uneven payments?

Answer: These formulas only work for equal, regular payments. If you have varied payment amounts, use the present value formula separately for each individual cash flow and sum the results.

Question: How should I adjust the formula if interest compounds monthly, but payments are yearly?

Answer: Adjust both the interest rate and the number of periods so that they match the frequency at which the interest actually compounds, not just when you make payments.

Question: What’s the difference between an annuity and a perpetuity?

Answer: An annuity ends after a set number of payments, while a perpetuity pays the same amount forever. The perpetuity formula is easier—just PMT divided by the interest rate.

Question: Are there any online tools or apps that help with annuity calculations?

Answer: Yes! Most banks, brokerages, and financial sites offer free annuity calculators. Plus, Excel and Google Sheets have easy-to-use built-in formulas for these equations.

How Annuity Formulas Can Shape Your Financial Decisions

Learning to calculate annuity values puts you in the driver’s seat for financial decisions. For instance, figuring out present value helps you decide if taking a lump-sum lottery win today is smarter than collecting payments over thirty years. Calculating the future value of steady savings lets you see how small, consistent steps can build a sizable nest egg over time. It makes things like buying a home, choosing loan terms, or preparing for retirement less mysterious, giving you the confidence to make moves that work for your goals.

Whether you’re planning to save, borrow, or invest, annuity formulas give you a clear lens to examine your options and compare offers side by side. Over time, these basic calculations can help you achieve more security and peace of mind, making your longterm goals not just dreams but real possibilities within your reach.